Canada’s economy relies on the little guy: 98.6% of all businesses in Canada are considered ‘small’, having fewer than 100 employees, and these employ 62.3% of the entire workforce. These businesses also account for just under half of the country’s GDP, SMEs contributed an average of 47.2% of private sector GDP over the 2018-2022 period, with small businesses alone contributing 33.2%. So it’s no exaggeration to say that the success of Canadian small businesses is paramount to the success of the country.

But there has been a lot of economic and geopolitical turbulence in 2026, threatening these small businesses, and in some cases providing opportunities to thrive. Keeping track of the ever-changing landscape is key to avoiding the former while capitalizing on the latter. So here we’re going to delve into the most important issues, trends, challenges and opportunities facing Canadian small business owners in 2026, starting with the state of these businesses as they stand.

Where Are We Now?

The majority of Canada’s businesses are small, but within that basic definition (meaning fewer than 100 employees), there is quite a lot of scope. 59.1% of Canadian small businesses have fewer than 5 employees. And as you can imagine, the challenges and opportunities seen by a business of 4 people can be quite different to those seen by a business of 90 people. So when we talk about Canada’s small businesses, we need to be aware of this range, and know that the majority of private small businesses in Canada have just a handful of employees.

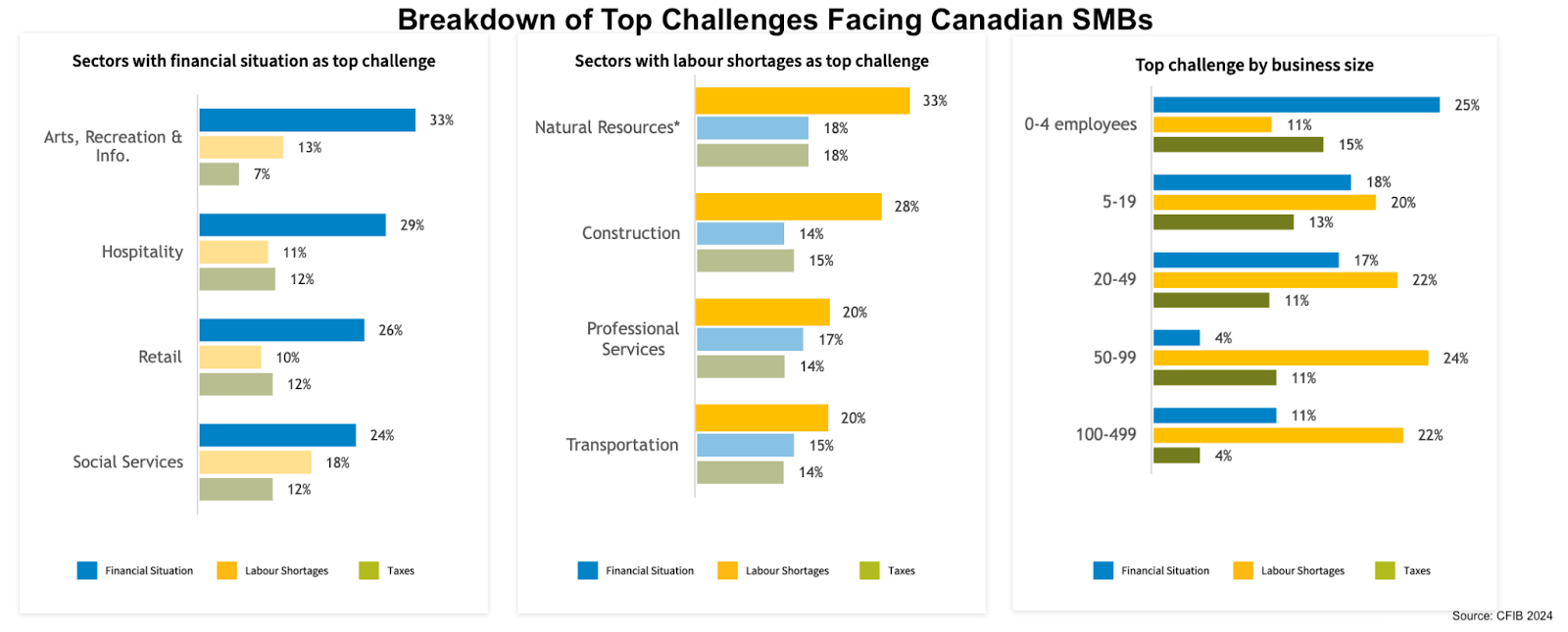

This isn’t uniform across industries though; in fact, the size of business is heavily dictated by industry. Nearly half of all small businesses in Canada are in just four sectors: professional, scientific and technical services; construction; retail trade; and health care and social assistance.

In addition, there are geographic variations. While Ontario, B.C., Alberta and Quebec are home to the most small businesses, on a per capita basis the picture looks very different. There are disproportionately more small businesses in Western Canada and the Territories than elsewhere in the country.

So now we know how many small businesses there are in Canada, where they are, and which industries they’re in. But how are they doing?

Major Challenges for Small Businesses in 2026

U.S. Tariffs & Trade War

Since early 2025, escalating U.S. tariffs have become the single biggest challenge facing Canadian small businesses. What began as 25% tariffs on non-CUSMA-compliant goods quickly expanded to steel, aluminum, lumber, autos and more, disrupting supply chains that Canadian businesses have relied on for decades.

The impact has been severe: according to CFIB research, 63% of small businesses report higher expenses as a direct result of tariffs, 53% have seen reduced profits, and 48% report lower revenue. Supply chain disruptions affect 42% of businesses, and over a third have paused investment plans entirely.

Perhaps most concerning is the uncertainty. 79% of business owners say unpredictable tariff policy is a barrier to planning, and 75% say the trade war has increased their stress levels. By Q3 2025, Canadian exports were 4% lower than pre-tariff levels overall, with some sectors hit far harder.

The federal and provincial governments have responded with support measures including work-sharing programs, tariff remission processes, and sector-specific funding. A ‘Buy Canadian’ movement has also gained momentum, with provinces removing U.S. alcohol from liquor store shelves and prioritising Canadian-sourced procurement

Feeling the squeeze from rising costs and trade uncertainty? BizFund provides quick, flexible cash advances to help Canadian small businesses navigate challenging economic conditions. No lengthy bank applications — apply today and get funded fast.

Research shows that the smaller the company is, the bigger the problems it faces, and this was especially true during the pandemic. Unfortunately, many of these problems have persisted even with the lifting of pandemic-related restrictions, leading to continued slow business growth for small companies. Small businesses are still seeing lower revenues, higher debt loads and weaker employment figures – despite medium and large businesses recovering more quickly.

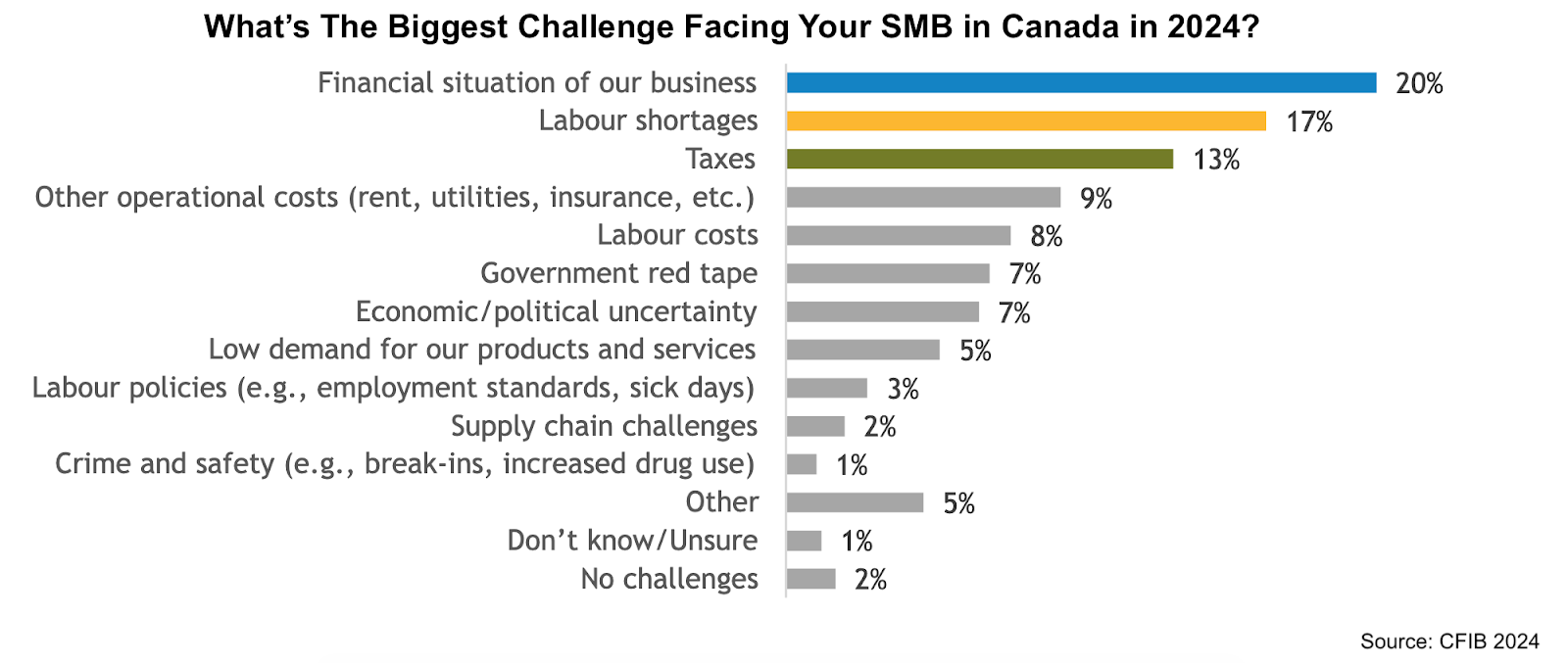

More than any other, businesses cite two major challenges to their operations in 2026: financing, and labour.

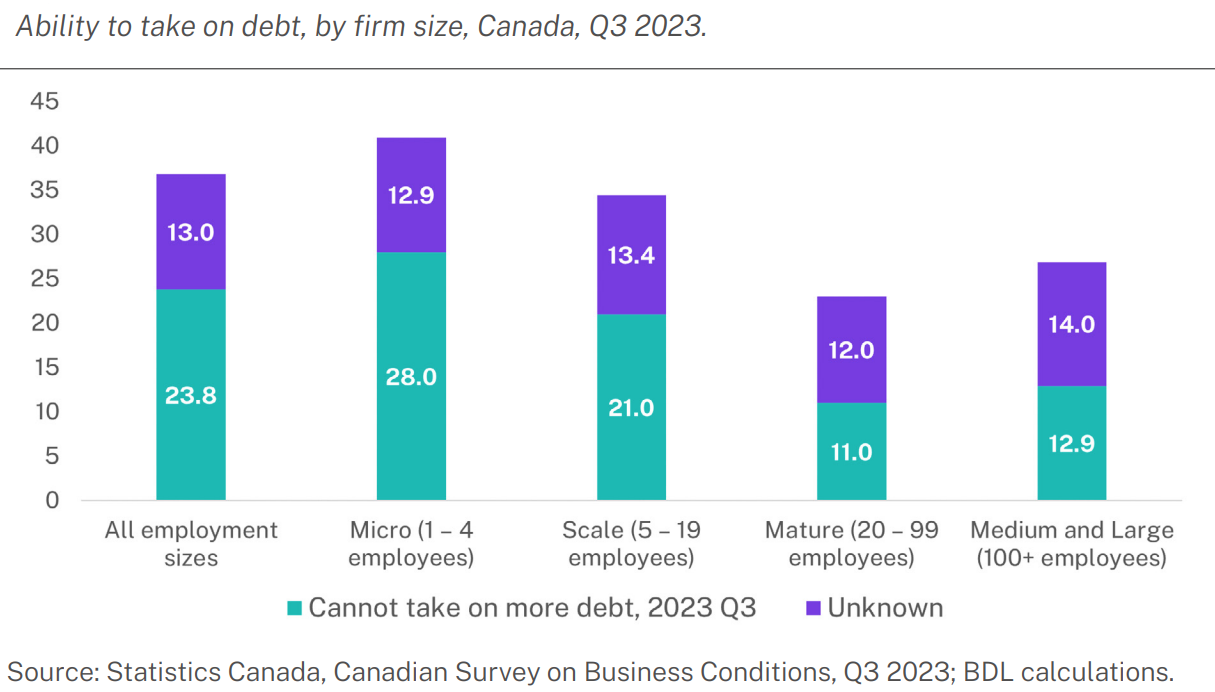

While the Bank of Canada has been cutting interest rates through 2025, the relief has been slow to reach small businesses. According to Statistics Canada, businesses with 1-19 employees remain more likely to report that interest rates have had a high impact on their operations, with 15.5% reporting a high impact and a further 21.8% reporting a medium impact.

Add to this the cost pressures from tariffs and rising operational expenses, and many small businesses find themselves squeezed from multiple directions. Over 20% cite cash flow concerns as a primary issue heading into 2026.

Struggling to get financing for your small business? BizFund can help with quick and easy access to cash advances. Click here to find out more.

Labour shortages, while still present in certain sectors, have eased somewhat heading into 2026. Canada’s unemployment rate rose to 7.1% through 2025, loosening the labour market. Statistics Canada’s Q4 2025 survey found that smaller businesses were actually less likely to expect labour-related challenges than larger firms.

Instead, insufficient domestic demand has emerged as the top constraint. CFIB’s December 2025 Barometer noted that more than half of businesses report demand as their primary growth obstacle, a shift from the labour-first concerns of 2023-2024.

These aren’t the only challenges facing Canadian small businesses. Inflation, tax burdens, economic uncertainty, demand, and supply chain issues are all also prevalent; but despite all this, business owners are overwhelmingly optimistic.

A Look At Business Owners’ Perception

Business confidence has been on a recovery trajectory. The CFIB Business Barometer long-term index reached 59.9 in December 2025, a three-year high, before slipping slightly to 59.5 in January 2026. While this is near the historical average, it masks significant variation: confidence is stronger in Ontario, Alberta and B.C., while short-term optimism remains subdued across all provinces.

70% of small businesses remain optimistic about the year ahead, though many are tempering expectations. As CFIB chief economist Simon Gaudreault noted, ‘the economy is still fragile heading into 2026.’

So while times are tricky, many small business owners are using the opportunity to pivot and grow their business in new ways.

Major Trends for Small Businesses in 2026

There are a number of ways Canadian business owners can adapt to changing consumer and economic needs and capitalize on new opportunities. Being aware of the most prevalent and popular trends is key to choosing which to tackle. Here’s what’s shaping up for 2026 and beyond for Canadian small businesses:

A Continued Drive To Online

83% of Canadian retail shoppers do online research before visiting a store. The level of online shopping post-pandemic has not fallen to pre-pandemic levels, so businesses with user-friendly digital platforms – especially mobile compatible – are capturing more revenue than those without.

This is true of marketing as well; consumers increasingly expect digital marketing tools and promotions and 70% favour companies offering them over those who prioritize physical or in-person strategies.

Digital Improvements Across Operations

It’s not just about improving or expanding the sales experience; digital transformation can occur across all aspects of a business, and more than half of small businesses who have implemented digital changes note that they improved profitability. Collaboration tools, supply chain optimization, cloud computing, security measures and task automation can all significantly improve operations, and those failing to exploit the advantages of new technologies risk becoming obsolete.

The adoption of new technologies isn’t happening evenly across businesses though; different industries, and perhaps more interestingly, different sized businesses have varying preferences. Generally speaking, the larger the firm, the more likely they are to invest in digital improvements. This is likely an effect of capability rather than desire though.

If your small business needs some help with its digital adoption, try the Canada Digital Adoption Program.

Artificial Intelligence Is Not Just For Tech Companies

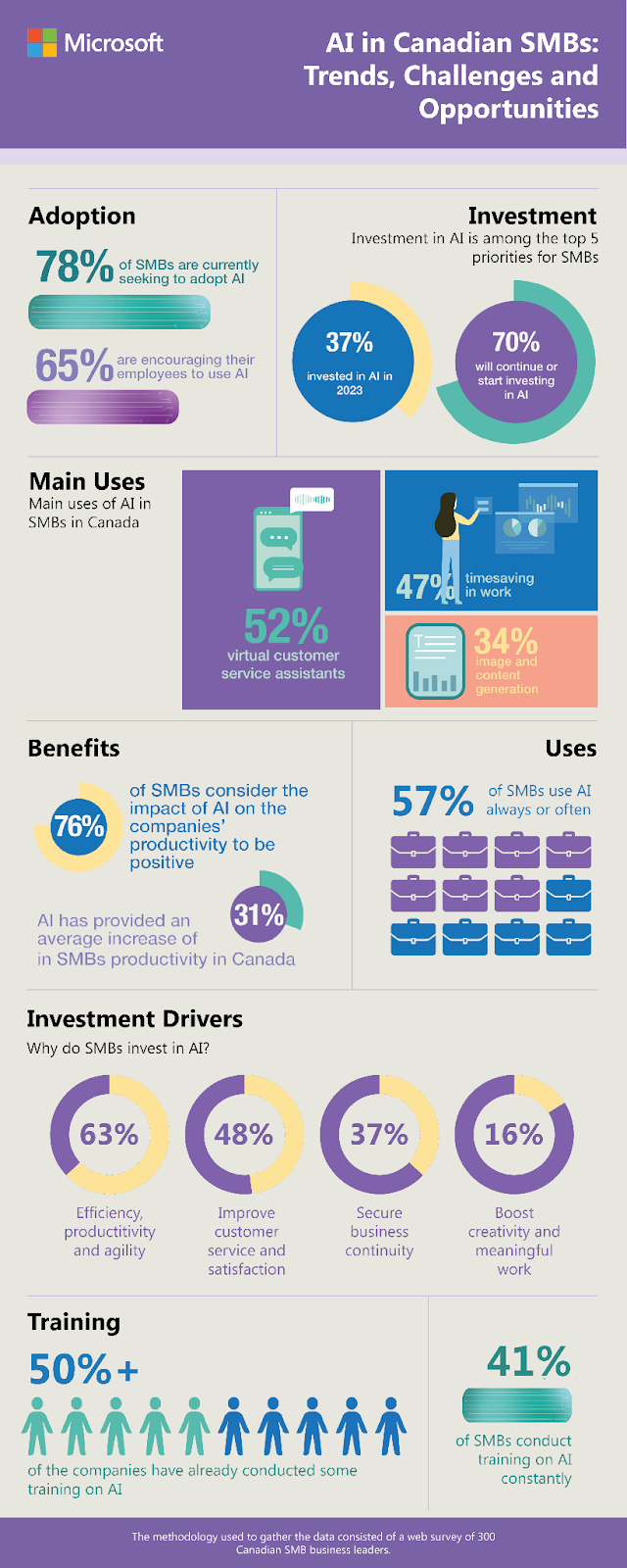

AI adoption among Canadian businesses has doubled in just one year. Statistics Canada reports that 12.2% of businesses used AI to produce goods or deliver services in 2025, up from 6.1% in 2024. But a Microsoft-commissioned survey paints an even more dramatic picture: 71% of small and medium-sized businesses now actively use AI or generative AI tools in their operations, with adoption reaching 90% among digitally mature firms.

The productivity gains are real. CFIB research found that SMEs using generative AI save an average of 1.08 hours per day, effectively doubling their productive time for every hour spent with AI tools. For every $1 invested in digital tools, businesses see $1.60 in return on average, rising to $2.40 for those who have fully integrated technology across their operations.

However, a gap remains between adoption and deep integration. While 92% of small businesses use digital tools in some form, only 10% have fully integrated them across operations. And despite 93% of larger organisations using AI, only 2% report seeing a clear return on their AI investments so far. The opportunity is clear, but realising it requires moving beyond experimentation.

Nearly 75% of Canadian SMEs plan to increase their AI investment, with 63% prioritising generative AI. Key applications include customer service chatbots, marketing automation, data analytics and document processing. For small businesses operating with tight margins and limited staff, these tools can level the playing field against larger competitors.

If your small business needs some help harnessing AI, try the AI Assist Program from the NRC Industrial Research Assistance Program.

Sustainability Matters Everywhere

61% of consumers believe that companies should put more emphasis on the environment and sustainability; 49% believe that companies must reduce their environmental impact, even if it means charging higher prices; and 56% have stopped buying from companies whose business practices they don’t agree with.

Small businesses are driven by sales, so understanding that sustainability is now a decision-critical factor for many consumers is key to a business aligning with their needs. What this looks like practically depends on the industry, but failure to appreciate the scale of this driver in consumer behaviour will only lead to future revenue decline.

Don’t Ignore DEI

Diversity, equity and inclusion (DEI) is, like sustainability, a growing decision-critical factor in consumer behaviour. 53% of Gen Z consumers want proof of how companies are acting on DEI, and they can get the data they need to make informed decisions. For example, several provinces have passed pay transparency legislation aimed at promoting pay equity. This affects labour too, as job applicants are more able to determine a business’s DEI practices and thereby choose one that matches their priorities.

Creating and adopting a DEI strategy may seem onerous for small businesses, but there are resources available to help. Check out the Business Development Bank of Canada’s DEI toolkit as a place to start.

Buy Canadian Movement

One of the most significant consumer shifts in 2025-2026 has been the ‘Buy Canadian’ movement. Fuelled by frustration with U.S. trade policy, Canadians have rallied behind domestic businesses in unprecedented ways. Provinces removed American alcohol from liquor store shelves, retailers began prominently labelling Canadian-made products, and consumer preference for Canadian brands surged.

For small businesses, this represents a genuine opportunity. Companies that can clearly communicate their Canadian identity, through branding, sourcing and community involvement, are finding receptive consumers willing to pay a premium to keep dollars in Canada. CFIB has even created ‘Proudly Canadian Owned’ materials for businesses to display at point of sale.

Trade Diversification

With 86.6% of Canadian goods exporters selling to the United States, the tariff shock has underscored the risk of over-reliance on a single market. More businesses are exploring diversification, Canada has 15 free trade agreements covering 51 countries, yet most small businesses have never exported beyond the U.S. Programs from Export Development Canada and the Trade Commissioner Service can help SMEs identify and enter new markets, turning a crisis into a catalyst for longer-term resilience.

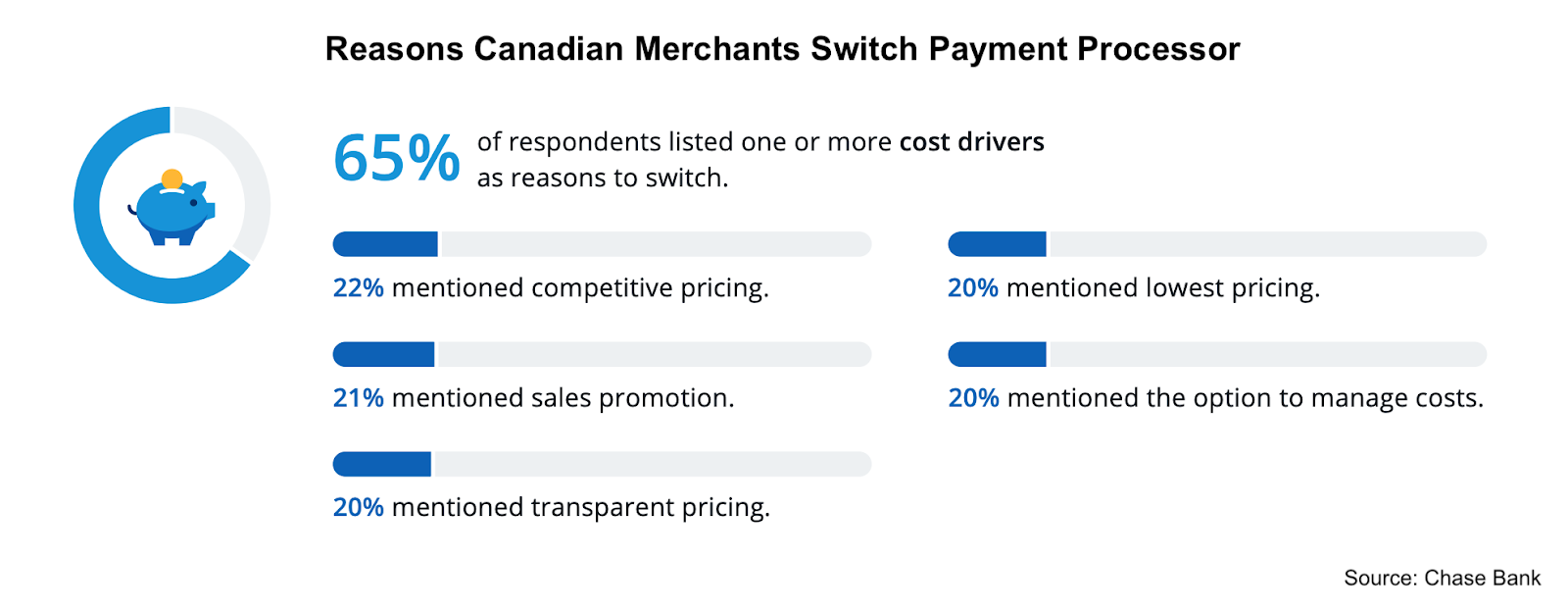

Payment Methods Are Changing

There has been a flurry of new payment methods in recent years, and businesses need to understand which are preferred in order to retain business. Those that have gained ground in Canada include mobile wallet, contactless credit card, and buy-now-pay-later. But consider: 88.1% of Canadians have smartphones, but only 51% of businesses accept mobile wallet payments. Among those businesses that do accept them, mobile wallets make up nearly half (47%) of all received payments. Clearly, the capacity to accept the payment methods preferred by consumers is crucial to competitiveness.

A compounding factor here is payment processing fees. 79% of small business owners state the cost of accepting credit card payments is unsustainable, and transaction fees across platforms and vendors are coming under scrutiny. 86% of business owners say they are open to switching their payment vendor. This, combined with novel payment methods, means businesses need to consider both consumer and operational needs when choosing their future payment systems.

An Aging Population Means More Acquisitions

Here’s an astonishing fact: about 10% of small businesses in Canada will be sold to external parties by 2025 thanks to retiring business owners. This will heavily impact the acquisitions market; and as businesses that grow through acquisition are twice as likely to experience above-average sales growth as businesses who grow organically, this presents a unique opportunity.

Economic realities must be met though, and funding an acquisition via traditional debt is not perceived to be the smartest move right now. Alternative financing options that mitigate the impact of high interest rates is preferable for those hoping to grow their business while avoiding financial risk.

The Bottom Line

While many experts believe the economic volatility of the past few years is largely behind us, for any small business to continue to survive in our changing world it needs to prioritize adaptability. The speed with which new technologies, new consumer priorities and new challenges can emerge mean that small businesses who remain nimble have a much greater chance of success.

If you’re interested in keeping your retail business, hospitality business or healthcare business ready for anything, talk to BizFund to find out how merchant cash advances can help with a variety of needs.

For Canadian Business Owners

Need capital to keep growing?

A Merchant Cash Advance gives you fast access to business funding based on your revenue — no lengthy bank process, no fixed monthly payments. Over 10 years helping Canadian businesses move faster.

No obligation. No bank visit required.