Did you know that 78% of business loan applications to Canadian banks are declined? These time-consuming, often difficult applications can be crucial to a business’s future, so making sure you put your best foot forward is key. Here we break down what you need to know to prepare a successful loan application.

1. Always Check Eligibility Rules

Before applying for any loan, you must check that your business meets the lender’s eligibility requirements – otherwise you are simply wasting your time. Different lenders can have different requirements, but most will ask for:

- A minimum business credit score

- A minimum personal credit score for the business owner(s)

- Detailed company information

- Company financial statements for at least the past 6 months, and possibly up to the last 2 years

- Cash flow and income records and projections

- Evidence of business assets and other collateral

- A detailed business plan

2. Improve Your Credit Score

Typically, lenders require a business credit score of 650; this can be lower (e.g. if your business has collateral to secure the loan), but it can also be higher if the lender is worried about risk (e.g. if the business owner has a poor credit history).

One of the best ways to boost your loan application’s chance of approval is to proactively protect and improve your credit score. You can do this by:

- Paying all bills on time

- Setting up pre-authorized payments wherever possible

- Making sure that you make at least the minimum payments on credit products

- Never missing a bill payment; if you fear you won’t be able to make a payment, contact the supplier/lender before it becomes due to work out a resolution

- Establishing a long history of credit

- Not using all of the credit available to you – only using what you need to keep your credit utilization ratio low

- Limiting the number of new loan and credit applications you make at any one time

To understand more about business credit scores and how they’re calculated, read our article on the topic here.

3. Write a Killer Business Plan

Your reasons for applying for a loan and how it will be used to improve your business’s success are also very important. This – and many other pertinent aspects of your business – should be covered in a comprehensive business plan.

A good business plan should contain:

- An executive summary with a brief description of the business and loan request; this document should contain all the most crucial information, so it can be used as a quick reference tool

- A full description of the company including history, corporate structure, current operations and products/services, wider industry, and primary competitors

- Personnel information highlighting the experience of the managerial staff and organizational structure of the business

- Key financial data, including income statements, cash flow statements, balance sheets, budgets and bank statements

- Market analysis addressing the company’s products/services (including lifecycle, development information and business model), the company’s client base, its position in the industry, the wider industry’s outlook, economic factors that may affect success, information on competitors, and so on

- Financial projections for at least the term of the loan being applied for

- Marketing/sales plan that indicates how the company will sell its products/services, its client base, and its competitive advantage

- A funding request that details exactly how much money is being applied for, its intended use and anticipated effect on the business

The best business plans are professional, thorough and well-organized. Remember to include a table of contents and numbered pages for ease-of-use (and if submitting documents digitally, bookmark appropriately), check formatting and layout for readability and consistency, and include your company’s logo and contact info on the cover.

4. Include Supporting Documents

As well as the wealth of information needed for a comprehensive business plan, it’ll help your loan application if you include documents that support your business assumptions and assertions. These are best placed in an appendix to your business plan, and can include:

- Market studies/research supporting your forecasts/conclusions

- Client testimonials

- Tax returns (business and personal)

- Business insurance information

- Details on existing leases (e.g. copy of commercial lease)

- Media reports about your company/industry

- Principals’ resumes

- Evidence of business assets e.g. real estate documentation

- Analysis of why the type of funding being applied for was chosen versus other options (and to learn about all of your possible business financing options, check out our ultimate guide)

5. Avoid Common Mistakes

Lastly, there are some red flags that lenders know to look out for, so be sure to avoid:

- Waiting until the last minute to apply for funds – a reliable business owner will be proactive about their future needs

- Making trivial mistakes on loan forms or failing to supply the requested information

- Not having a detailed plan for the loan funds

- Making large business changes right before applying for a loan, so that your business’s historical info is less relevant

- Submitting disorganized or unclear documents; your company’s professionalism will be judged by the quality of your submitted paperwork

If In Doubt, Remember the Five Cs

There are five categories commonly used to summarize how a lender assesses a loan application, known as the five Cs. These are a great reference if you’re struggling to understand how your loan application will be viewed:

- Character – documented behaviour that indicates how financially reliable you are

- Capacity – your company’s budget and cash flow i.e. ability to meet loan terms

- Capital – funds available for contingencies, so loan repayment is more likely even if your company encounters difficulties

- Conditions – economic or industry conditions that may impact cash flow and therefore repayment

- Collateral – assets available to pledge against a loan to reduce the lender’s risk

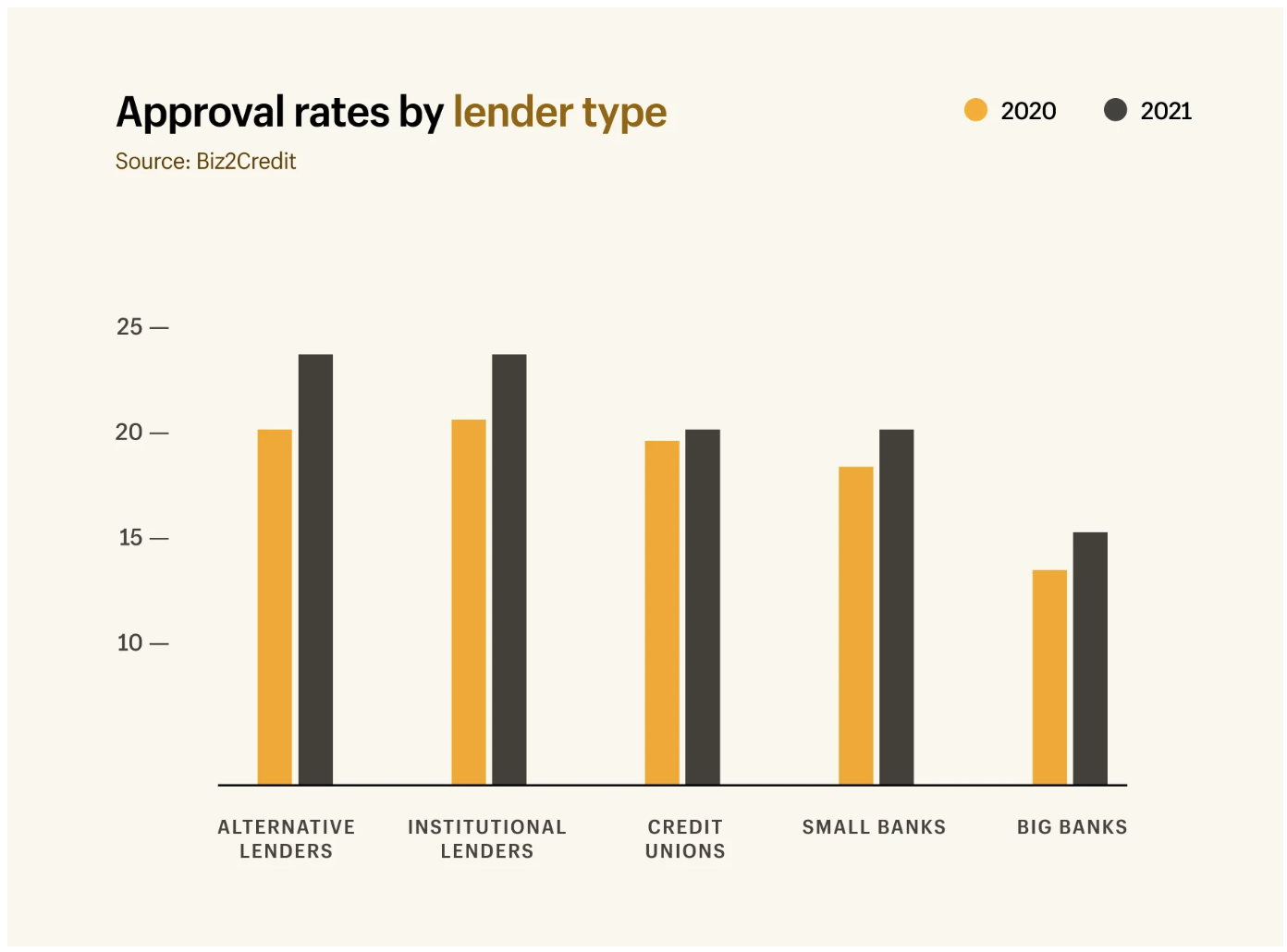

If you’re in need of business financing and are worried about banks’ low approval rates, connect with BizFund to find out what your alternative options are.

For Canadian Business Owners

Need capital to keep growing?

A Merchant Cash Advance gives you fast access to business funding based on your revenue — no lengthy bank process, no fixed monthly payments. Over 10 years helping Canadian businesses move faster.

No obligation. No bank visit required.