As a business owner, there are many aspects of your business’s finances that you have to keep track of, and amongst the day-to-day of budgets, invoices, balance sheets and payroll, you may overlook something vital: your credit score. A business’s credit score has an enormous impact on its ability to function, so to make sure you’re doing everything you should be, read on!

What Is a Business Credit Score?

Just like people, every business has its own credit score. This is a number that represents a business’s credit worthiness, based on its past financial behaviour, and is used by lenders and other financial providers – of all types – to judge how reliable a company is, and how likely it is they will meet their debt obligations.

The higher the score, the more financially trustworthy a business is deemed to be, and the easier it will be for that business to obtain loans and other credit products. Businesses with high credit scores also have access to better rates and deals.

How To Find Your Business Credit Score

Unlike with personal credit scores, which run from 300 to 900 regardless of which credit bureau is used, business credit scores are not standardized. There are multiple business credit bureaus, and each uses their own system and their own metrics to calculate scores – so you may find your score differs between bureaus.

This can make accessing and understanding your business credit score more challenging. However, there are a couple of providers that cover the majority of the Canadian business credit rating market, so just staying on top of these is sufficient. They are:

Equifax

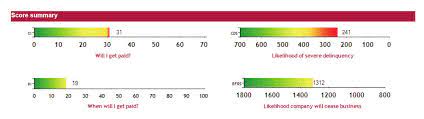

Equifax is one of the biggest credit agencies in Canada, and its credit reports for businesses have four different ratings on them, each with its own scale:

To get a copy of your report from Equifax, you need to create a login on their website and purchase one; the fees are not advertised, so you have to speak to a representative from Equifax to get a price.

TransUnion

TransUnion is Canada’s other major credit bureau, and it uses a three digit credit scoring system, as with personal scores. You can access your TransUnion credit report via their website’s business portal, but again, they do not publicly state the cost to do so.

Dun & Bradstreet

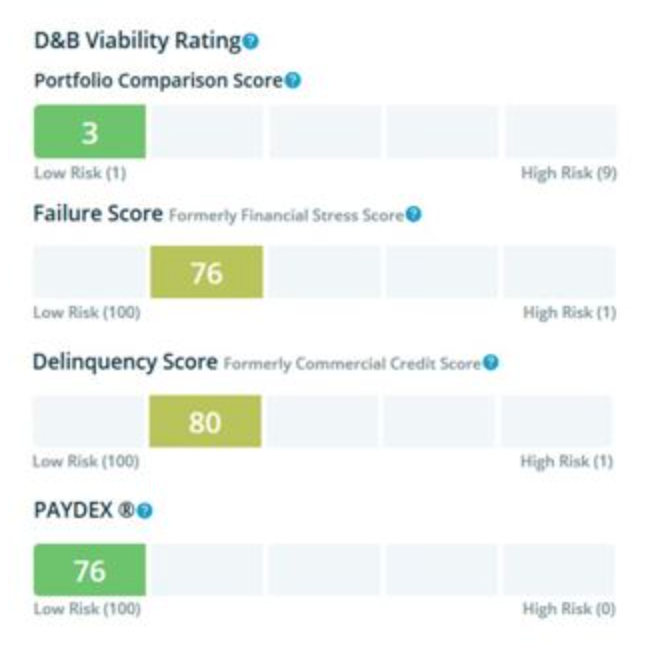

Dun and Bradstreet is another option for Canadian businesses; their credit reports also have multiple scores on them, representing different areas of risk. Businesses can access their Dun and Bradstreet report on their website; they are the only bureau that offers a free option, although there are also paid options for those in a hurry or requiring more detail.

Experian

Experian offers a tiered approach to accessing reports, with one-time access costing just $40, and premium access to multiple reports costing $2,000 for a year. They also have multiple metrics for rating businesses, although they do distill this into a single ‘score summary’ for simplicity and quick comparisons. You can access your Experian report here.

How Are Business Credit Scores Calculated?

Although Canadian credit bureaus use different methods and metrics in their calculations, all will look at essentially the same underlying information when determining a business’s score:

- Business’s age

- Business background information, such as ownership

- Credit history, including types and amounts of credit used

- Payment history of bills/debts

- Amount of outstanding debt

- Types of credit in use and age of existing credit

- Recent credit applications

- Changes in credit activity over time

- Credit utilization ratio

- Public records regarding liens, lawsuits, bankruptcies, etc.

- Business risk factors

- Industry risk factors

- Business competitors and industry trends

Why Does Your Business Credit Score Matter?

You might think that the lack of standardization across Canadian business credit scores means they are less important than personal credit scores, or that you can afford to ignore them. This is far from the case; every time your business applies for financing, with any lender, your credit profile and score will be assessed and used as a key metric in determining whether or not you get approved. A good credit score means easier loan approvals, lower interest rates, higher borrowing amounts, and sometimes even cheaper insurance rates too.

And, crucially, a business’s credit score and report is publicly available to anyone, as long as they pay the fee. So unlike consumer credit reports, which are protected by regulations regarding consumer privacy, any client, vendor, or member of the public can see your business’s credit score and use it to judge whether or not they want to deal with you.

How To Improve Your Business Credit Score

There are some simple ways to keep on top of your business’s credit score:

- Check your credit score often

- Immediately report any errors or inconsistencies

- Pay all of your bills on time

- Set up automatic payments

- Keep your credit utilization low

- Prioritize credit accounts with providers that report financial activity to the credit bureaus

- Improve your personal credit score

- Make sure your business and personal credit use is properly separated

- Ensure negative items drop off your credit report when resolved

- Establish trade accounts with your suppliers

- Only use the credit you need and stay current

- Do not make new credit inquiries unless necessary

The Bottom Line

Almost every company will need access to business funding at some point – and even those that don’t still rely on suppliers and clients who may check a company out before dealing with them. So make sure you stay on top of your business credit score, in order to keep your business healthy over the long-term. And if you need any help accessing financing for your business, regardless of your credit, speak to one of BizFund’s experts.

For Canadian Business Owners

Need capital to keep growing?

A Merchant Cash Advance gives you fast access to business funding based on your revenue — no lengthy bank process, no fixed monthly payments. Over 10 years helping Canadian businesses move faster.

No obligation. No bank visit required.